Carbide tools are indispensable in many machining processes—rising raw material prices have a direct impact on costs and availability.

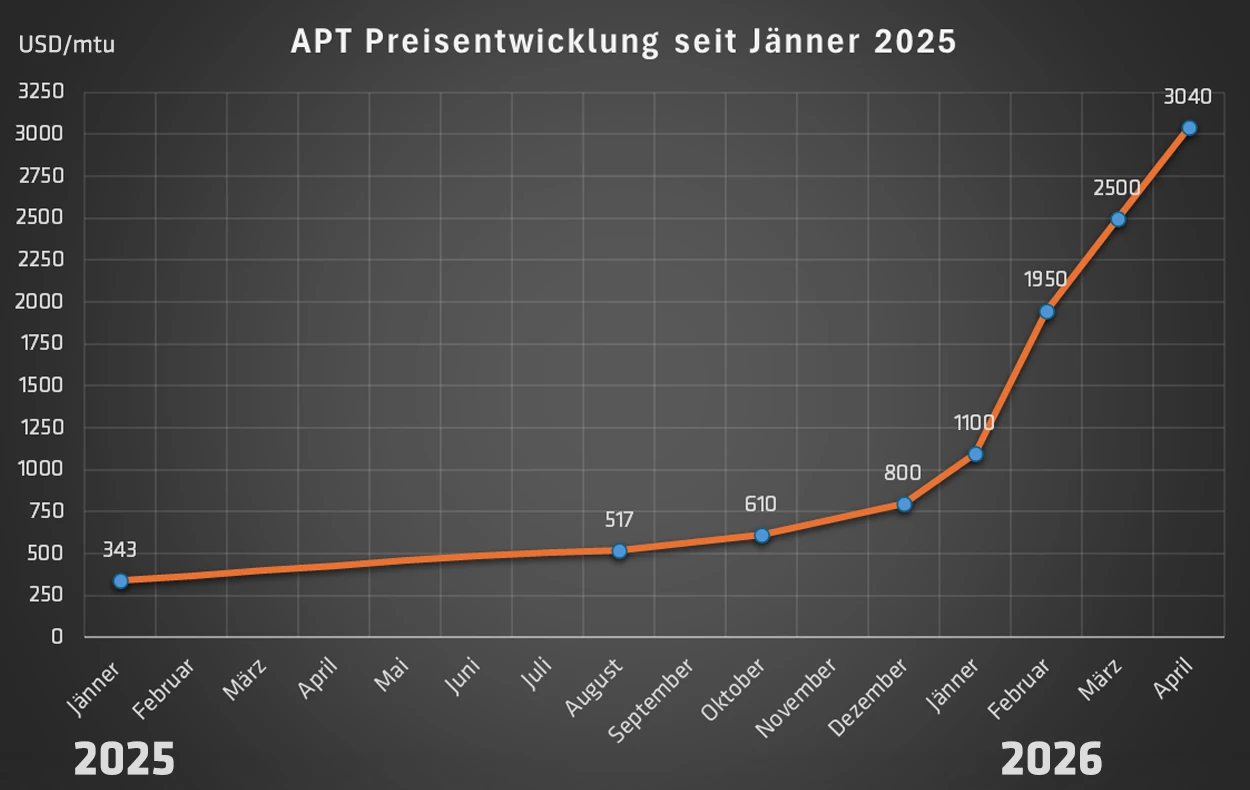

Since January 2025: The price of tungsten has skyrocketed!

Raw material prices for cemented carbide have fluctuated significantly in recent months and are now at a level that poses major challenges for manufacturers and users. Particular focus is on tungstenraw materials and cobalt as a typical binder metal. This development affects not only purchase prices, but also entire manufacturing processes, supply security, and cost structures in metalworking.

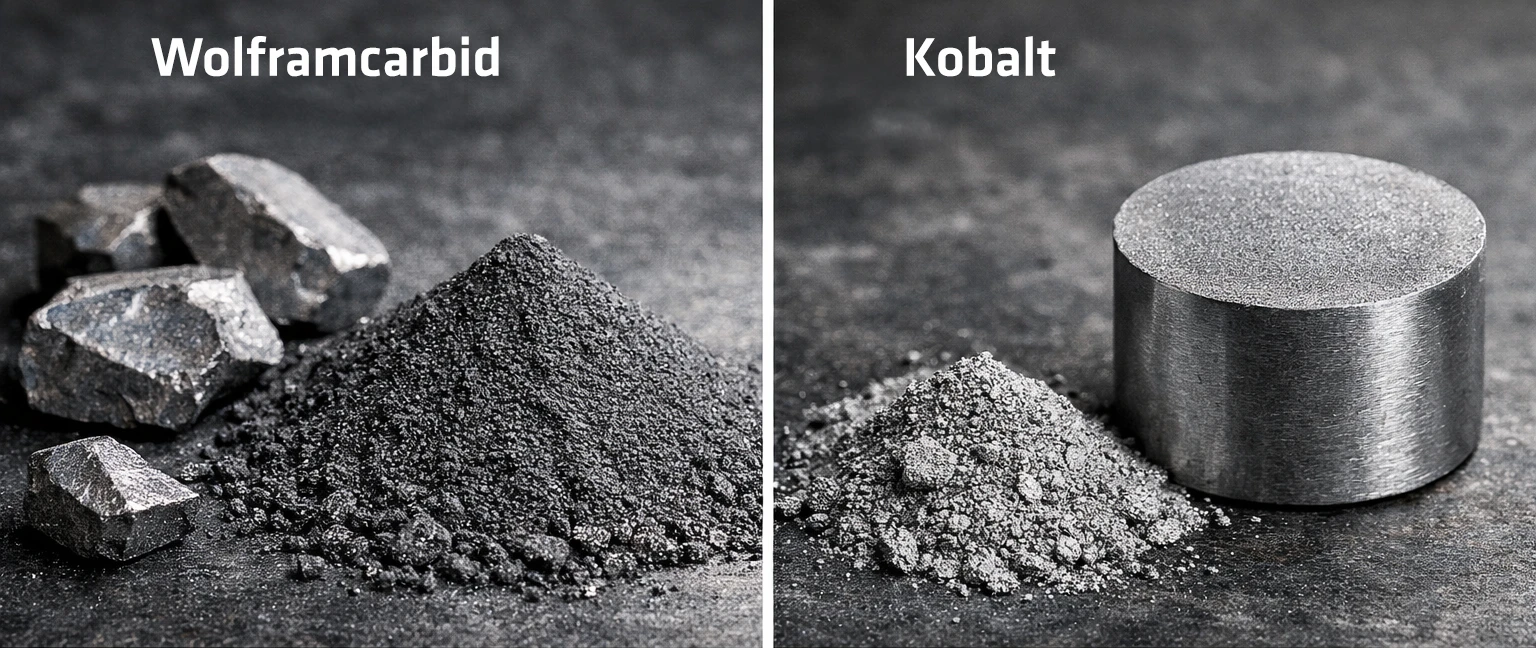

Hartmetall ist der dominierende Schneidstoff in vielen Zerspanungsanwendungen. Wendeschneidplatten, Vollhartmetallwerkzeuge und Sonderlösungen für professionelle Fertigungsprozesse werden nahezu ausschließlich aus diesem Material hergestellt. Technisch besteht Hartmetall überwiegend aus Wolframcarbid (WC), während Kobalt als Bindemittel zum Einsatz kommt.

Beide Rohstoffe werden an den globalen Metall- und Rohstoffmärkten gehandelt und unterliegen sowohl Preis- als auch Verfügbarkeitsrisiken. Steigen die Rohstoffpreise, wie in den vergangenen Monaten, wirkt sich das unmittelbar auf Werkzeugkosten und Lieferfähigkeit aus – sei es durch höhere Einkaufspreise, längere Lieferzeiten oder strengere Beschaffungsbedingungen.

Wolframpreise seit 2025: steiler Aufwärtstrend

Seit Anfang 2025 steigen die Preise für Wolfram deutlich. Ammoniumparatungstat (APT), eine wichtige Vorstufe von Wolfram, wird häufig als Referenzwert für die Preisentwicklung von Wolfram verwendet. Zu Beginn des Jahres 2025 lagen die Preise noch auf einem moderaten Niveau.

Durch eine Kombination aus exportpolitischen Maßnahmen, Angebotsengpässen und steigender globaler Nachfrage kletterten die Preise innerhalb eines Jahres stark nach oben. Handels und Rohstoffanalysen berichten, dass sich Wolfram-Preise 2025 im Jahresverlauf annähernd verdreifacht haben und 2026 noch erheblich steiler ansteigen.

Kobalt

ist neben Wolfram ein weiterer wichtiger Rohstoff in vielen Hartmetallen, dient hier aber meist als Bindemittel. Die Preisentwicklung bei Kobalt zeigt ebenfalls Anstiege, jedoch stabilisiert sie sich mit weniger dramatischen Preisbewegungen im Vergleich zu Wolfram.

Obwohl Kobaltpreisschwankungen zu einem gewissen Teil ebenfalls zu den Beschaffungskosten beitragen, ist es aktuell vor allem Wolfram, das preislich den globalen Rohstoffmarkt für Hartmetallwerkzeuge dominiert.

Tungsten prices have not only risen; they have undergone a complete structural shift.

Causes of price pressure in the tungsten market

The reasons for the rapid price changes are varied and go beyond simple supply-and-demand dynamics:

1. China’s Dominance in the Tungsten Market

China is by far the world’s dominant producer of raw tungsten. According to industry publications, the vast majority of global tungsten production comes from China, and since 2025 the country has tightened regulations on its export and production policies, which has significantly reduced supply for international buyers.

Economics as a lever: In the middle of the year, China introduced new export controls requiring government approvals for numerous tungsten products. At the same time, export volumes fell significantly, leading to a supply shortage in international markets.

2. Supply side under pressure

In addition to export restrictions, reduced production quotas, stricter environmental regulations, and declining production capacity in some regions are limiting the available volume.

3. Strong demand from industries such as defense, mining, and aviation

Another structural factor is rising demand from strategic industries. Tungsten is needed in critical applications such as high-performance materials, defense technologies, and high-temperature components—areas where demand is rising sharply in some cases.

The downward pressure on tungsten prices stems not only from demand but, above all, from geopolitical dependencies, export restrictions, and structural supply constraints.

Recommendations for Users

Given the trends in raw material prices, companies in the machining industry should consider the following strategies:

1. Long-term procurement planning

Supply contracts with stable terms, larger safety stock levels, and early ordering cycles can help mitigate price spikes.

2. Recycling as a strategy

Tool recycling continues to gain economic importance: By recycling carbide scrap, companies can lower raw material costs and reduce supply chain burdens.

3. Tool reconditioning / Regrinding

Regrinding carbide tools can extend their service life and allow raw materials to be reused multiple times. This not only reduces material consumption but also helps lower the cost per component and maintain stable production levels during periods of high raw material prices.

4. Process and Tool Optimization

By consistently designing tools, cutting parameters, and machining strategies with specific applications in mind, tool life can be extended and costs per part reduced—a decisive advantage when raw material prices are high.

Why recycling is so important!

Recycling carbide scrap in the EU strengthens the supply of raw materials and reduces dependence on Chinese imports.

Sustainability and independence:

In times of geopolitical uncertainty, rising resource nationalism, and volatile trade dynamics, a stable supply of raw materials in Europe is becoming increasingly important. In the case of tungsten, the recycling of carbide scrap plays a central role in this regard.

Making Europe more independent: Ceratizit, part of the Austrian Plansee Group and one of the largest tungsten suppliers in the Western world, reports that it uses approximately 91% recycled tungsten in its cemented carbide production. The European recycling facilities are located in Austria and Finland. There, the environmentally friendly thermal zinc process is used, which enables high material quality while simultaneously reducing dependence on the Chinese raw materials market. It is therefore particularly important to keep carbide scrap as a source of raw materials in Europe and to recycle it here as well.

-

- Thermische Behandlung von gebrauchtem Hartmetall mit Zink

- Recyceltes Pulver enthält über 99 % des Wolframcarbids in seiner ursprünglichen Form

- Kosteneffizienter im Vergleich zu chemischen Verfahren

- Umweltfreundlich, da keine Nasschemie erforderlich ist

Umweltfreundlich: Recyceltes Wolfram ist deutlich umweltfreundlicher als primär durch Bergbau gewonnenes Material: Rund 75 % geringerer Energiebedarf und etwa 40 % weniger CO₂-Emissionen sprechen eine klare Sprache. Parallel dazu wird kontinuierlich an noch effizienteren und ressourcenschonenderen Recyclingverfahren gearbeitet. Aus diesen Gründen ist das Recycling von Hartmetallschrott in europäischen Anlagen ein zentraler Baustein für die langfristige Ressourcenverfügbarkeit und eine geringere Abhängigkeit von geopolitisch unsicheren außereuropäischen Lieferketten.